Featured

Table of Contents

Adapting to High-Interest Environments in Major Metro Areas

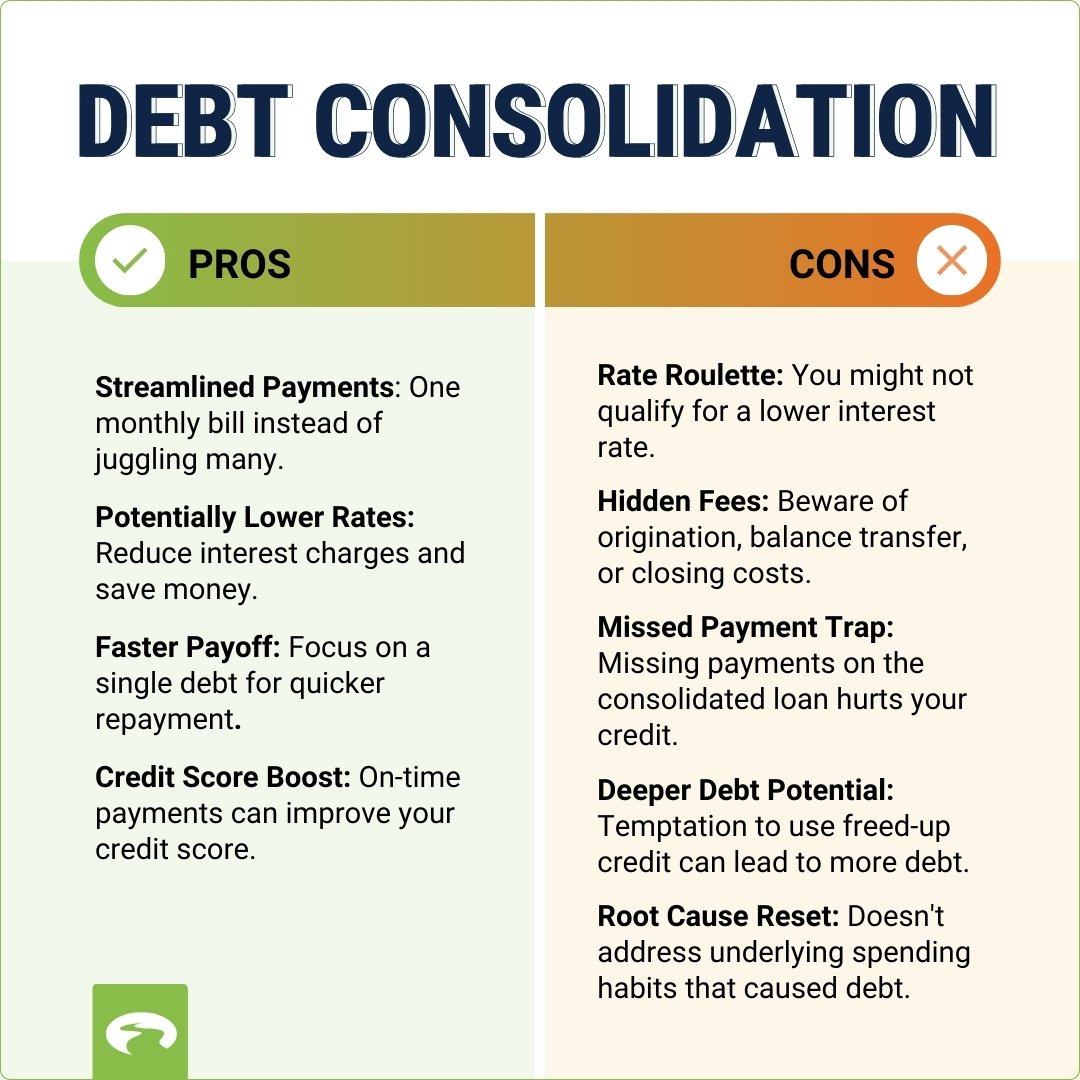

Charge card balances in 2026 have reached levels that require more than simply minimum payments. For numerous homes in urban centers, the increasing expense of living has squeezed monthly margins, resulting in a rise in revolving debt. Handling these balances involves more than simply budgeting-- it requires a tactical shift in how interest is handled. High interest rates on charge card can create a cycle where the primary balance barely moves regardless of consistent payments. Professional analysis of the 2026 monetary environment recommends that rolling over financial obligation into a structured management strategy is ending up being a basic move for those seeking to gain back control.

The existing year has actually seen a shift toward more official debt management structures. While debt consolidation loans were the primary option in previous years, 2026 has actually seen an increase in using nonprofit debt management programs. These programs do not include securing a new loan to settle old ones. Rather, they concentrate on restructuring existing responsibilities. Success in financial obligation decrease often begins with expert competence in Financial Education. By working with a Department of Justice-approved 501(c)(3) nonprofit company, individuals can access settlements that are normally not available to the general public. These firms work directly with creditors to lower rates of interest and waive late costs, which enables more of each payment to approach the primary balance.

Mechanics of Debt Management Plans in 2026

A financial obligation management program functions by combining numerous regular monthly charge card payments into one single payment made to the counseling agency. The firm then distributes these funds to the different lenders. This system streamlines the process for the customer while guaranteeing that every lender receives a payment on time. In 2026, these programs have actually become more advanced, often incorporating with digital banking tools to supply real-time tracking of financial obligation reduction development. For locals in various regions, these services provide a bridge between frustrating debt and monetary stability.

The settlement phase is where the most substantial cost savings happen. Lenders are frequently going to provide concessions to not-for-profit agencies since it increases the possibility of complete payment. These concessions may include dropping a 24% rates of interest down to 8% or lower. This decrease substantially alters the mathematics of financial obligation repayment. Professional Credit Card Relief supplies a clear roadmap for those dealing with several lenders. Without these negotiated rates, a customer may spend decades paying off a balance that could be cleared in 3 to five years under a handled strategy. This timeline is a crucial element for anyone planning for long-term goals like homeownership or retirement.

Comparing Debt Consolidation Loans and Nonprofit Therapy

Picking between a debt consolidation loan and a debt management strategy depends on credit health and current income. In 2026, credit requirements for low-interest individual loans have tightened. This leaves many people in different parts of the country searching for options. A debt consolidation loan is a brand-new financial obligation that settles old financial obligation. If the rate of interest on the brand-new loan is not significantly lower than the average of the credit cards, the benefit is minimal. If the underlying costs routines do not change, there is a danger of running up the credit card balances once again while still owing the combination loan.

Nonprofit credit counseling companies offer a various technique. Because they are 501(c)(3) organizations, their primary focus is education and financial obligation reduction rather than revenue. They supply free credit therapy and pre-bankruptcy counseling for those in alarming straits. Discovering reliable Payment Reduction in Montana can indicate the distinction between insolvency and healing. These firms likewise manage pre-discharge debtor education, guaranteeing that individuals have the tools to prevent duplicating previous errors. This educational part is typically what separates long-lasting success from temporary relief.

The Role of HUD-Approved Real Estate Counseling

Debt management does not exist in a vacuum. It is carefully tied to housing stability. In the local market, many people find that their credit card debt prevents them from getting approved for a mortgage or even keeping current rental payments. HUD-approved real estate therapy is a essential resource provided by across the country companies. These services help people understand how their financial obligation affects their real estate options and provide methods to secure their homes while paying for lenders. The combination of housing recommendations with debt management produces a more steady monetary foundation for households across the 50 states.

In 2026, the connection in between credit rating and real estate costs is tighter than ever. A lower debt-to-income ratio, attained through a structured management strategy, can lead to much better insurance coverage rates and lower home mortgage interest. Therapy companies frequently partner with local nonprofits and community groups to make sure that these services reach diverse populations. Whether in a specific territory, the goal is to supply available financial literacy that equates into real-world stability.

Long-Term Technique and Financial Literacy

Rolling over financial obligation in 2026 is as much about education as it is about rate of interest. The most effective programs include a deep focus on financial literacy. This involves discovering how to track expenditures, build an emergency fund, and comprehend the mechanics of credit rating. Agencies that run across the country frequently use co-branded partner programs with banks to assist customers shift from debt management back into standard banking and credit items. This transition is a significant milestone in the recovery procedure.

Using independent affiliates helps these agencies extend their reach into smaller neighborhoods where specialized financial recommendations may be limited. By offering these resources in your area, they ensure that assistance is offered no matter location. For those in surrounding areas, this implies access to the same high-quality therapy found in major financial. The method for 2026 is clear: stop the bleeding by lowering rates of interest, combine the procedure to make sure consistency, and utilize the resulting cost savings to develop a long-term monetary safeguard.

Managing financial obligation is a marathon. The 2026 environment requires a disciplined approach and a determination to look for expert guidance. By making use of the structures supplied by not-for-profit agencies, people can browse the complexities of modern credit. The procedure of moving from high-interest revolving financial obligation to a structured, worked out plan is a proven path to monetary health. With the best assistance and a concentrate on education, the financial obligation that seems unmanageable today can be a distant memory within just a few years.

{kind=link}

Latest Posts

What Every Borrower in Your Area Needs to Know

Does Credit Therapy Hurt Your Score in Your State?

How Kansas City Kansas Citizens Utilize Equity for Financial Liberty